Car Insurance Fronting occurs when the main driver of a car declares someone else as the main driver (usually a parent) to reduce the cost of their insurance premium. Fronting is illegal and can result in the cancellation of your car insurance policy, a fraud conviction or both.

Why Do Drivers Front?

New or young drivers usually commit fronting because they traditionally pay higher car insurance premiums.

Young drivers are considered a higher risk, which results in higher car insurance premiums.

Due to this increase, some young drivers try to reduce their insurance premiums by setting up an insurance policy in an older, low-risk driver’s name and adding themselves as a named driver. Sometimes, they may not even realise what they are doing is fraudulent.

Why is Fronting Illegal?

Car insurance premiums are calculated based on the driver’s risk of claiming in the future. The higher the risk of a claim, the higher the premium is. Insurance companies take many different factors into account when calculating a premium. For example, if a driver has had no claims for more than 5 years, KennCo reduces their premium by up to 64%. Their chances of claiming are much lower based on their driving history.

Therefore when a driver with more experience pretends that they are the main driver to reduce the cost when the main driver is a high-risk candidate, the policy premium is not a true reflection of the risk involved.

What Happens If Drivers Front?

It may be tempting to risk fronting if you receive high insurance quotes. However, it isn’t worth it in the long run. Fronting may void your car insurance, meaning that your insurer may not pay for any damage to your car if you make a claim. As well as being left to foot the bill in case of a claim, you may also be charged with insurance fraud. Having a criminal conviction can also hurt the price of your car insurance in the future. So the potential savings are not worth the risk.

The Psychology Behind Fronting

Many young drivers, eager to hit the road but deterred by high insurance premiums, might consider fronting as a solution. However, it’s crucial to recognise the long-term implications of such a decision:

Immediate Savings vs. Long-Term Costs: While fronting might offer immediate savings, the long-term costs, both financially and legally, can be substantial.

The Role of Peer Pressure: Sometimes, young drivers might consider fronting because they know someone who’s done it or because they feel it’s the only way to afford driving. It’s essential to resist such pressures and make informed decisions.

Cheaper Car Insurance for Young Drivers

At KennCo, we are committed to helping young drivers get on the road to becoming safe and responsible drivers. We now offer own and named driver insurance policies to anyone aged 17 and over, and we also take into account any named driving experience you may have. Call KennCo for a quote today on 01 409 2600.

Driving can be expensive for those starting off between the ages of 17-24. Parents may want to help by putting themselves as the main driver and adding their child as a named driver. They and their children are committing fraud and are breaking the law by doing so.

Is car insurance fronting illegal in Ireland?

Yes, car insurance fronting is illegal in Ireland. It is considered a form of insurance fraud and can result in serious consequences, including criminal charges, fines, and the loss of your insurance coverage.

What happens if I am caught fronting on my car insurance in Ireland?

If you are caught fronting on your car insurance in Ireland, you may face serious consequences. Your insurance company may cancel your policy, refuse to pay out on any claims, and report you to the authorities. You may also face fines, criminal charges, and the possibility of a criminal record.

How can I avoid being accused of car insurance fronting in Ireland?

To avoid being accused of car insurance fronting, it is important to be truthful when filling out your car insurance application. Make sure to accurately list all drivers of the vehicle, including yourself, and do not list any driver as a primary driver if they are not.

How Can Younger Drivers Get Cheaper Insurance?

For young or less experienced drivers, it can be worth considering the type of car you drive and the impact on your car insurance. We’ve compiled a list of cars that are cheaper to insure here. At KennCo, we also take into account any named driving experience you may have when providing a quote.

Save On Young Driver Car Insurance?

At KennCo, we understand that it can be hard for young drivers to get their first car on the road. That’s why we offer low-cost and reliable young driver car insurance.

Headlights are not just a feature of your car; they are a critical safety tool that, when used properly, significantly enhances visibility and communication with other road users. This guide delves into the correct usage of car headlights, with a focus on the important role of your car’s dipped headlights.

Understanding Car Headlights

Car headlights come in two primary settings: main (or full) beam headlights and dipped headlights. Each serves a specific purpose, adapting your vehicle for optimal visibility and safety under different driving conditions.

Main Beam Headlights

Main beam headlights provide a bright, direct light that illuminates the road ahead over long distances. However, their intensity can dazzle oncoming traffic, making them suitable for use only when no other vehicles are in front or coming towards you, typically on unlit roads.

Dipped Headlights

Dipped headlights, on the other hand, are designed to offer good illumination without causing glare to other road users. They are angled downwards and are the most frequently used lighting setting, essential for most driving conditions during the night and at times of reduced visibility.

Daytime Running Lights

In addition to the main beam and dipped headlights, modern vehicles are often equipped with Daytime Running Lights (DRLs). These were introduced to increase safety by helping to make vehicles more noticeable during the day and in conditions where visibility may be reduced – such as at dawn, dusk, or in poor weather conditions.

DRLs automatically activate when the engine is started. They typically illuminate the front of the vehicle only – and do not illuminate the road ahead or the rear of the vehicle. And while they play a crucial role in enhancing daytime safety, they are not a substitute for dipped headlights in poor driving conditions or during the night.

When Should a Driver Use Dipped Headlights

During Low Light Conditions

Dipped headlights should be used from dusk till dawn, ensuring your vehicle is visible to others even as natural light fades. They’re crucial during the early morning and late evening hours, or when overcast weather conditions reduce visibility.

During Bad Weather

Fog, heavy rain, and snow can significantly reduce visibility. In such conditions, dipped headlights can make your vehicle more visible to others, while also improving your own view of the road.

In Tunnels and Underpasses

Even during the day, tunnels and underpasses can be significantly darker than outside conditions. Switching to dipped headlights helps make your presence known to other drivers navigating these shared spaces.

On Busy Streets

In urban and built-up areas, especially during twilight hours or when street lighting is insufficient, dipped headlights help in highlighting your vehicle among the myriad of road users, including pedestrians and cyclists.

Compliance with Road Safety Regulations

Irish road safety regulations mandate the use of dipped headlights during certain times and conditions to ensure not just your safety, but also that of others on the road. Familiarising yourself with these rules is not just about avoiding penalties; it’s about contributing to a safer driving environment for everyone.

Tips for Effective Headlight Use

Regular Maintenance

Ensure your headlights are clean and functioning correctly. Dirt and grime can significantly diminish their effectiveness, while a faulty bulb can compromise your visibility and safety.

Avoiding Glare

Be mindful of other road users and switch from main beam to dipped headlights when encountering oncoming traffic or driving closely behind another vehicle.

Using Automatic Settings

Many modern vehicles come equipped with automatic headlight settings that adjust according to external light conditions. While convenient, it’s important to manually override these settings when necessary to ensure optimal lighting.

Headlight Distance

While dipped headlights improve visibility, they have their limitations, especially in terms of distance illuminated. Adjust your driving speed accordingly to ensure you can stop within the area lit by your headlights.

Using Your Car Headlights

The correct use of car headlights, especially dipped headlights, is a fundamental aspect of safe driving in Ireland. By adhering to the guidelines outlined above, drivers can ensure not only their own safety but also that of others on the road.

Remember, headlights are not just for seeing but for being seen. As the evenings draw in or whenever visibility is compromised, make the switch to dipped headlights as a standard part of your driving routine. For a fast, reliable car insurance quote, reach out to one of our trusted KennCo Insurance advisors on 01 409 2600, or click here for a quick online quote.

Car Headlights: When To Use Dipped Headlights Frequently Asked Questions

When exactly should a driver use my dipped headlights?

Drivers should use dipped headlights in low-light conditions, including the hours between dusk and dawn, early mornings and late evenings or during overcast weather; when driving in busy streets, urban areas or in tunnels/underpasses; and drivers should also use their dipped headlights during poor weather conditions like heavy rain, fog or snow to improve visibility.

Is it illegal to drive with only one working headlight?

Yes, driving with only one working headlight is illegal as it significantly reduces visibility and can be misleading to other road users. Ensure both headlights are functioning correctly.

How often should I check my headlights?

It’s advisable to check your headlights regularly, at least once a month, to ensure they are clean, correctly aligned, and fully functional.

When is it safe to use full beam headlights?

Full beam headlights are designed to light the road over long distances and should only be used on unlit roads when there is no oncoming traffic or vehicles directly in front of you. Because of their intense brightness, they can potentially dazzle and temporarily blind other road users.

What should I do if an oncoming car is using full beam headlights and dazzling me?

If dazzled by oncoming traffic, avoid looking directly at the lights. Instead, slow down if necessary and use the left edge of the road or lane markings as a guide until the vehicle has passed.

Can I use my main beam headlights in heavy fog?

No, it’s not recommended to use main beam headlights in heavy fog as they can cause glare, making it harder for you to see and for other drivers to see you. Use fog lights if your vehicle is equipped with them, or stick to dipped headlights.

Why do my headlights seem dimmer than they used to be?

Dimming can occur due to several reasons, including bulb age, dirty headlight covers, or incorrect alignment. Check these factors and replace or clean as necessary.

What are Daytime Running Lights (DRLs)?

Daylight Running Lights (DLRs) are a safety feature on modern cars designed to make your vehicle more noticeable during the day. They turn on automatically when the engine is started but generally only light the front of your vehicle. They do illuminate the road ahead or turn on your rear lights and are not a substitute for dipped headlights at night or in poor visibility.

Are daytime running lights enough in poor weather conditions?

No, daytime running lights are designed to make your car more visible to others during daylight hours and are not a substitute for dipped headlights in poor visibility conditions. Always switch to dipped headlights in reduced visibility to ensure safety.

Looking to Save On Your Car Insurance?

At KennCo, our car insurance cover offers competitive rates and valuable benefits, including a replacement car as standard. Get peace of mind knowing you’re fully covered.

Q. Understanding Car Insurance Claims in Ireland: Insurance Trends & Insights

A.

Understanding how car insurance claims work in Ireland is important for both customers and providers. There are a number of different factors and trends that affect car insurance claims and how they are processed here in Ireland. Below, we’ll take a more in-depth look at some of these trends to give you a better understanding of how they may impact your policy.

Car Insurance Claims Process in Ireland

Over the past number of decades, the car insurance claims process in Ireland has been shaped by various factors, including changes to legislation, demographic shifts and emerging technologies.

Types of Car Insurance Claims

Collision and Comprehensive Claims

Collision claims, resulting from accidents with other vehicles or stationary objects, are the most common type of claim in Ireland. Comprehensive claims, which cover events like theft, fire, and vandalism, are less frequent but significant, especially in urban centres where the risk of such incidents is higher.

Personal Injury Claims

Personal injury claims, though not as common as property damage claims, are a major concern due to their high cost. The introduction of the Personal Injuries Assessment Board (PIAB) and subsequent legislative reforms have been instrumental in standardising and expediting the process of these claims, aiming to reduce fraudulent practices and ensure fair compensation.

Factors That Influence Car Insurance Claims

The landscape of car insurance claims in Ireland has been shaped by various factors, including technological advancements, legislative changes, and demographic shifts.

Government Legislation

In recent years, the Irish government has implemented several legislative changes aimed at creating a more balanced and fair insurance market. Including stricter penalties for driving offences, reforms in the PIAB process, and initiatives aimed at creating greater transparency in insurance pricing. All steps towards stabilising the insurance market in order to protect consumers.

Changing Demographics

Young drivers, traditionally seen as high-risk, have shown a decrease in claim frequency which has been attributed to better driver education and awareness initiatives. However, the severity of claims involving this demographic still remains a concern, with many incidents involving younger drivers on the road often linked to high speeds.

Older drivers tend to be involved in fewer accidents. When accidents do occur, they are typically low-speed, minor collisions that often occur in urban settings.

Technology

New and emerging technologies also play a role in how car insurance claims are processed. Most modern cars now come equipped with infotainment systems and advanced driver safety features built-in. While these technologies are designed to keep you safe and have been shown to successfully reduce road traffic accidents, they can have an impact of the cost of an insurance claim if an accident does occur.

The increasing use of dashcams by motorists across Ireland is helping insurers to resolve claims, establish liability and detect fraud. Additionally, drivers and other road users who record dashcam footage of dangerous driving will soon be able to upload the footage to an online portal, under plans by the An Garda Síochána. It is hoped that the portal will be live in 2026 allowing other road users to submit footage that could then be looked at An Garda with a view to potential prosecution.

Seasonal and Regional Factors Influencing Insurance Claims

The Irish weather plays a role in insurance claims, with winter months seeing an increase in incidents due to shorter days and challenging weather conditions. This time of year often sees a rise in minor collisions and single-vehicle accidents.

In terms of regional differences, more densely populated urban areas like Dublin tend to experience a higher frequency of claims. This is primarily due to the increased number of vehicles on the road.

In contrast, rural areas tend to report fewer incidents, but often see more severe accidents. Likely due to higher speeds and less congested roads.

Future Trends In Car Insurance

The future of car insurance claims in Ireland is likely to be influenced by several key factors:

Impact of Autonomous Vehicles: The gradual introduction of autonomous vehicles is anticipated to lead to a decrease in collision claims. However, this may also introduce new types of claims related to technology failures or cybersecurity issues.

Climate and Weather-Related Claims: With the ongoing impact of climate change, there may be an increase in claims related to extreme weather events, such as flooding caused by storms. This may necessitate adjustments in insurance policies and coverage as a result.

Urbanisation Areas: As urban areas become more congested, the frequency of minor collision claims is expected to rise. This trend may prompt the need for insurance products specifically tailored to urban living conditions.

Car Insurance Trends in Ireland

The car insurance claims process in Ireland is constantly changing. For customers looking to take out a car insurance policy, it’s important to understand the different factors in order to make informed decisions about their car insurance.

For insurance providers, these insights are invaluable for developing policies that meet the evolving needs of Irish drivers. As the industry navigates these changes, a responsive, fair and forward-thinking approach is needed.

Contact KennCo for a secure, reliable insurance quote today. We will be happy to give you a quote or dicuss your options. Call 01 409 2600 today.

Looking to Save On Your Car Insurance?

At KennCo, our car insurance cover offers competitive rates and valuable benefits, including a replacement car as standard. Get peace of mind knowing you’re fully covered.

Q. What to Do After a Car Accident: Guide for Drivers and Young Drivers in Ireland

A.

Being involved in a car accident, even a minor one, can be overwhelming, especially for young, novice and inexperienced drivers. But knowing what steps to take after the incident can help you to stay calm, safe, and handle the situation correctly. This guide will walk you through the necessary actions to take if you’re involved in a minor car accident.

Stay Calm

While easier said than done, the first and most important thing to do is to stay calm. Stop, take a few deep breaths and steady your nerves. Panicking doesn’t help and will only make the situation more stressful.

Move to a Safe Location Provided it’s safe to do so, move your car to the side of the road to avoid blocking traffic, apply your handbrake and switch on your hazards. If you have one, place your warning triangle at the rear of your car to alert oncoming traffic that there has been an accident.

Check for Injuries Next, check yourself and any other passengers who are travelling with you for injuries. If there are other cars involved, check on the occupants to make sure everyone is okay. Call emergency services immediately by dialling 112 or 999 if there has been an injury, or if someone requires assistance.

Call the Gardai In Ireland, you are legally required to report the incident to Gardaí if there has been a road-traffic accident. If it’s a minor incident, Gardaí may choose not to attend but it’s important that it still be reported. Following the accident, Gardaí will create an official report with an incident number.

Collect Information from the Scene

Take some notes of the scene and record all important or minor details, such as:

Date and time of the incident

The position of the vehicles

Damage to all vehicles involved

Make and model of cars involved

Any visible injuries

Contact details of any witnesses

Road conditions and weather at time of incident

You can also use your smartphone to take pictures or video documenting the scene, the cars involved and any damage caused during the incident. If there are disputes further down the line, the information you gather from the scene can be hugely beneficial from an insurance or legal perspective.

Exchange Information

You should exchange insurance and contact details with the other driver at the scene; and provide your name, address and any requested personal details to Gardaí.

If the driver is uninsured, you should still follow the steps outlined above and immediately contact the Gardaí and your insurer. In Ireland, the Motor Insurers’ Bureau of Ireland (MIBI) is the body which compensates drivers who have been hit by uninsured drivers.

Contact Your Insurance

It’s highly important that you contact your insurer immediately to report the incident. They will ask for your insurance details and policy number and for details of the collision or accident.

You should provide your insurer with all the information you’ve gathered from the scene such as the other driver’s insurance details, registration, and contact information. And any other relevant information like photos you took from the scene and contact details for any witnesses.

The more information you provide the better. Even if you don’t plan on making a claim, the other driver might so it’s important to inform your insurer.

Tips for Preventing Accidents

Anticipation: Always drive carefully and be aware of your surroundings and anticipate the actions of other drivers on the road.

Avoid Distractions: Don’t use your phone while driving, and stay focused on the road.

Follow Traffic Laws: Stick to speed limits and road signs can significantly reduce the risk of accidents.

FAQs for What to Do After a Minor Car Accident

What should young drivers and drivers do immediately after a minor car accident?

Stay calm, check for injuries, move to a safe location, and exchange information with the other driver.

Do I need to report a minor car accident to the Gardaí?

Yes, especially if there are injuries or significant damage. Reporting can also help if there’s any dispute about the incident.

What information should I exchange with the other driver?

Names, contact details, vehicle registration numbers, insurance information, and details of the vehicles involved.

Why is it important to take photos at the scene?

Photos provide crucial evidence for insurance claims and any potential legal issues.

KennCo Insurance Services

Q. Long Haul Flight Tips & Essentials

A.

Long-haul flights can be daunting, especially for people who don’t travel much, are more to shorter hops or who have never flown long distances. Sitting in a airline seat for hours, battling jet lag and keeping yourself comfortable and entertained can make for a challenging journey.

So, whether you’re a seasoned traveller or a first-time flyer planning a holiday abroad, these long-haul flight tips will help make your next journey smoother and more comfortable. Here are some travel tips for long flights:

Dress comfortably

When you’re travelling on a long-haul flight, it’s essential to wear comfortable and breathable clothes. You want to avoid being stuck in tight or restrictive clothing considering you’ll confined to a small space for a few hours. Choose loose-fitting clothes made from soft, comfortable fabrics like cotton. These materials will help you stay cool and comfortable throughout the flight.

It’s also a good idea to wear layers to adjust your clothing according to the temperature on the plane. Bring a light sweater or jacket you can easily remove if you get too warm.

Bring a Travel Pillow and Blanket

Many airlines offer pillows and blankets for long-haul flights but they might not be as comfortable as ones you can bring yourself. While not quite your home comforts, bringing a travel pillow and blanket can help you get some much-needed rest during your flight.

Look for a compact, easy-pack pillow that still provides the support you need for your neck and head. A small, lightweight blanket can also help you stay warm and comfortable during the flight.

Pack Some Snacks

Airline food can be hit or miss. Bringing some healthy snacks like nuts, fruit or granola bars can help you stay satisfied throughout the flight. These snacks are also easy to pack and take up only a little space in your carry-on bag.

Avoid sugary snacks and foods high in salt, as these can dehydrate you and make you feel even more uncomfortable during the flight.

Stay Hydrated

Dehydration can make you feel tired and uncomfortable so drinking plenty of water during your flight is important. Plus, the air in the cabin is often dry which can make you feel even more dehydrated.

Make sure to drink water throughout the flight – and avoid alcohol and caffeine if possible which can dehydrate you even more. You can also bring a refillable water bottle to help you stay hydrated and most airlines will give out complimentary bottles of water to keep passengers hydrated.

Move Around

Sitting in one position for an extended period can cause stiffness and discomfort. Get up and stretch your legs every few hours, and do some simple exercises in your seat to improve circulation. You can do small stretches like ankle circles, leg lifts, and shoulder rolls to help you stay comfortable during the flight.

If the plane has an area for stretching or walking, take advantage of it for extra movement.

Entertainment

Long flights can get a little boring so having something to keep you entertained is important. Bring a good book, download movies or listen to music to pass the time.

Having something to keep you entertained during the flight can make time faster. Some airlines also offer in-flight entertainment systems with movies, TV shows and games. A lot of modern long-haul flights can offer in-flight Wi-Fi and streaming options but you check this with the airline beforehand and be prepared to make your own entertainment.

Sleep Aids

If you have trouble sleeping on planes, consider bringing sleep aids like earplugs or an eye mask. These can help you relax and fall asleep more easily during the flight.

Pack Long Haul Essentials in Your Carry-On Bag

Remember to pack some essential items from a toothbrush, toothpaste, eye mask, earplugs, and any needed medications. Having some hygienic items is an excellent way to feel fresh and healthy while on your long-haul flight.

Invest In Travel Insurance

If you’re planning a long trip or long-haul flight, travel insurance is an essential add-on that can protect you against unexpected disruptions to your travel plans. Research from the CCPC shows that 16% of Irish holidaymakers who took a foreign holiday between May and August 2025 experienced some form of travel issues. A comprehensive policy can protect you against things like flight cancellations, delays, missed departures and lost luggage; and can provide cover and support in the event of an accident or medical emergency – so unforeseen incidents don’t turn into costly setbacks.

When choosing your travel insurance, look for coverage that fits your specific needs. Review your situation, consider the type of trip you have planned, assess the contents and exclusions of the policy and compare the cost to the level of coverage offered. A well-rounded policy can provide some peace of mind and let you focus on enjoying your flight and holiday.

Preparing for a Long Haul Flight

The key to a successful long-haul flight is to prioritise your comfort and well-being, so don’t be afraid to take the necessary steps to make your journey as smooth as possible. Following the long-haul flight tips discussed in this blog you can make the most of your flight and arrive at your destination feeling refreshed and ready to explore.

Looking for Travel Insurance Travel Insurance You Can Rely On?

At KennCo, we offer affordable travel insurance for individuals, couples and families. Choose between multi-trip or single trip cover depending on your needs and budget – with low cost Annual Multi-Trip cover from just €91.84.

As we get further away from the long, grey days of January, most people will be starting to plan or book summer holidays or city breaks. We all look forward to escaping the grind of daily life for a couple of weeks or a long weekend; but sometimes your summer getaway can come at a serious price.

While the vast majority of trips abroad go off without a hitch, the unpredictable nature of travel means that a significant number of people still get caught out by unforeseen circumstances.

When you consider that, according to the research, Irish holidaymakers spend close to €2,500 on average on flights and accommodation, it goes from being a minor annoyance that puts you out to putting you out of pocket. That’s why it pays to check what you’re booking and always invest in travel insurance before you fly.

What Can Go Wrong When Booking a Holiday Abroad…

While it can be smooth sailing (or flying) for the majority of travellers, things can and do go wrong. The CCPC consumer helpline received almost 2,700 contacts about travel related issues across the whole of 2025.

And in their 2026 travel report, the CCPC found that between May and September 2025:

Consumers report spending on average €2,473 on their holidays.

16% of holidaymakers faced issues while away; most notably with flight delays (6%) or flights being rescheduled (5%).

Among all age groups, 18–24-year-olds were most likely to encounter issues, with 29% affected.

17% of 18-24 year olds had a flight that was delayed by 3 to 11 hours.

1% had to travel home early due to an emergency.

1% required medical care for illnesses while abroad.

One in three holidaymakers travelled without insurance and almost half of under 35s were not covered by travel insurance.

Of those who did travel without insurance, 48% said they didn’t think they’d need it for the trip; while 19% said they didn’t think it was worthwhile.

One in ten bought insurance after they bought their holiday.

For the 16% of holidaymakers who experienced issues, flight delays and rescheduled flights were the most common culprits. While this can seem like a relatively minor thing, sudden changes to your flight time can have a knock on effect and can potentially cause you to miss a connecting flight or get you a day or two late to your destination, for example.

Another major headache affecting flyers is lost luggage. Aside from being inconvenient, it can also leave you shortchanged with the report highlighting a complaint where a traveller’s suitcase was lost by an airline during a skiing trip. As a result, they did not have their ski gear when they arrived and were unable to attend two ski lessons they had paid for in advance, leaving them out of pocket.

Other issues reported by consumers to the CCPC included day trips and tours being cancelled providers; accommodation being cancelled; illnesses that required medical treatment; and having to leave early due to emergencies.

The CCPC are also warning Irish holidaymakers about potential scams and misleading online offers. Listing some of the issues reported by consumers, the CCPC highlighted examples where a consumer paid out thousands of Euros to secure accommodation through a legitimate looking website only to find that it was a scam; in a similar instance, their 2025 Travel Scams Report highlights a case study where a consumer booked a holiday to France via an online travel agency. After paying €11,000 to cover the cost, the agency and website disappeared leaving the customer out of pocket and unsure if they could recover their money.

Other examples shared by the CCPC include a holidaymaker who booked accommodation based on an image of a sunny beach in the hotel’s advertising only to arrive and find out the beach was a four-hour round trip away!

Travel Insurance Gaps

One key thing that the CCPC research highlights is that a significant number of people are travelling without insurance or taking out insurance after the fact, and leaving themselves open to risks. With 30% of holidaymakers travelling abroad without insurance between May and August of last year, the time period recorded in the report.

This number increases for younger travellers with almost half (48%) of those under 35 choosing to go without cover. Which is unfortunate as 18-24 year-olds are the most likely to encounter issues when travelling, but the least likely to buy travel insurance!

While 1-in-10 bought insurance after they bought their holiday meaning they may not have been fully covered for certain disruptions, such as strikes or extreme weather events.

If you travel without insurance, you need to be prepared for the unexpected and expect to be out of pocket if something does go wrong. And you should bear in mind that taking out insurance late or after you’ve booked may not necessarily mean you’re covered.

How to Protect Your Trip This Summer

The best way to safeguard your trip and cover yourself against any unforeseen events is to take out travel insurance. We always suggest taking out insurance at the same time you book your flights and accommodation, that way you’re covered from the outset.

At KennCo, all of our travel insurance policies cover cancellations, medical emergencies, lost luggage and more. Which means you can get on with relaxing and enjoying your holiday, instead of worrying about potential problems or hiccups.

And whether you’re going on one summer holiday or planning multiple getaways throughout the year, we’ve got you covered with single trip, multi trip and family travel policies to make sure you have the right coverage at the best price. Outside of travel insurance, there are some other ways that you protect yourself when travelling abroad this summer.

Be wary of random or too good to be true offers, especially from unsolicited emails or social media ads.

Always do your research before booking. Look at review sites like Trustpilot and Google to make sure websites or providers are legitimate.

Always read the terms and conditions. And fully review the refund and cancellation policies before booking.

Only pay through secure channels or checkouts using a credit or debit card so you have some protection if things go wrong.

What to Consider When Buying Travel Insurance

Choosing the right travel insurance means picking a policy that suits your trip and the specific risks involved. While price is obviously a factor, it’s not necessarily about choosing the cheapest or most expensive cover, it’s about choosing the cover that protects you best.

Generally speaking, a comprehensive policy that covers cancellations, lost luggage, medical emergencies, and repatriation is usually ideal for most people. But you should also factor in specific event coverage if you’re planning any risky activities like rock-climbing, skiing or water sports.

Equally, you should check that your policy has adequate medical coverage and repatriation back to Ireland. If the worst does happen, you might find that foreign medical costs can add up quickly. Check that your policy will cover A&E visits, hospital stays, outpatient care and even emergency evacuation.

Travel Insurance from KennCo

Don’t let the threat of flight delays, lost luggage or unexpected emergencies ruin your holiday this summer. Taking a few minutes to secure the right cover can potentially save you thousands of euros and a massive amount of hassle if things do go wrong.

So, before you pack your bags for your next great adventure, secure your trip with KennCo Insurance. We focus on the risks so that you can focus on the journey. Get a quick and easy quote for KennCo travel insurance today.

Based on a research report by the Competition and Consumer Protection Commission (CCPC) looking at issues experienced by Irish holidaymakers who took a foreign holiday between May and August 2025.

CCPC report findings based on 1,012 telephone interviews with consumers conducted between 17-30 September 2025.

CCPC report analysis based on a respondent sub-group who took a holiday abroad between May and August 2025. The sub-group consisted of 419 respondents aged 18+.

The Competition and Consumer Protection Commission (CCPC) received 45,000 calls in 2024 with less than 1% related to a scam or potential scam.

CCPC Scam Report based on a sample of 30 respondents who contacted the CCPC helpline between May and August 2025. With the fraud or suspected fraud having occurred between November 2025 and August 2025.

Respondents were contacted by the CCPC via telephone survey and asked about their experience, and any resolutions.

Low-Cost Travel Insurance You Can Rely On

KennCo offers some of the best and most competitive travel insurance options for individuals, couples and families in Ireland. Choose between multi-trip or single trip cover and pick coverage that suits your needs. Get a quick quote online.

What are the most common issues experienced by holidaymakers?

Flights being delayed or rescheduled are among the most frequent complaints reported by consumers according to the CCPC. Other issues for Irish travellers include lost luggage and problems with accommodation.

When is the best time to take out travel insurance?

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat.

Who is most at risk when travelling abroad?

According to research from the CCPC, travellers aged between 18-24 are the most likely to encounter issues while travelling. The same report also found that, despite this risk, they are also the least likely to purchase holiday cover which leaves them highly vulnerable in the event of any problems or medical issues.

What should I look for when choosing travel insurance?

A comprehensive policy should cover things like cancellations, medical emergencies, lost luggage and repatriation. You should also check that your medical cover includes things like hospital stays and emergency evacuation. And remember to add specific coverage if you plan to do any risky activities like skiing or water sports.

Do many people travel without insurance?

According to research by the CCPC,1-in-3 holidaymakers travelled abroad without insurance in 2025. With 48% of travellers aged under 35 not covered by travel insurance while away.

Q. What Does Car Written Off Mean? Guide to Write Offs

A.

Everyone who is involved in a car accident may go through trauma. They have the potential to result in severe financial losses in addition to physical harm. A car’s damage may occasionally be so bad that it is labelled a “write-off.” But what does it mean exactly when a vehicle is declared written off? We will cover the fundamentals of what it means when a car is written off and your alternatives if it is involved in an accident.

What Does Car Written Off Mean?

A car is considered a write-off if the cost of repairing it is greater than a certain percentage of its worth. By not fixing the car, the insurance provider will instead pay the car’s market value, less any excess or deductible.

When a car is involved in an accident, it is assessed by an insurance assessor to determine the extent of the damage. If the car’s repair cost exceeds a certain percentage of its value, it is deemed a write-off. This means the insurance company will pay out the car’s value, minus any excess or deductible, rather than repairing it.

What Are the Categories of Car Write-Offs?

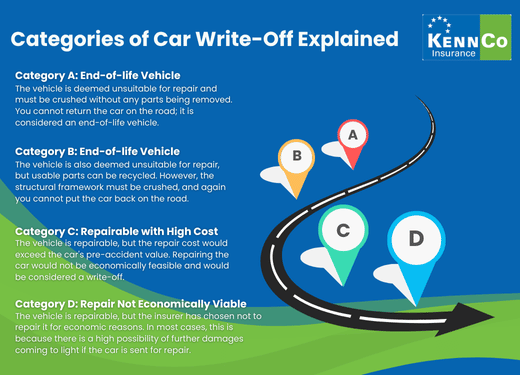

Car write-offs are divided into different categories depending on the severity of the damage. The categories are as follows:

Category A: End-of-life vehicle

The vehicle is deemed unsuitable for repair and must be crushed without any parts being removed. You cannot return the car on the road; it is considered an end-of-life vehicle. This category is reserved for severe cases where the car is beyond repair.

Category B: End-of-life vehicle

The vehicle is also deemed unsuitable for repair, but usable parts can be recycled. However, the structural framework must be crushed, and again you cannot put the car back on the road. This category is for cars that are too damaged to be repaired safely but still have some valuable parts that a garage can salvage.

Category C: Repairable with high costs

The vehicle is repairable, but the repair cost would exceed the car’s pre-accident value. Repairing the car would not be economically feasible and would be considered a write-off. However, if the car is repaired, it can return to the road.

Category D: Repairable but not economically viable

The vehicle is repairable, but the insurer has chosen not to repair it for economic reasons. In most cases, this is because there is a high possibility of further damages coming to light if the car is sent for repair. However, if the car is repaired, it can return to the road.

It’s important to note that write-offs are recorded on the car’s history and can affect its resale value. Furthermore, cars in categories A and B can’t be returned on the road, even if repaired. Therefore, it’s essential to understand the categories of car write-offs and their implications.

What Happens to a Car Once it is Written Off?

When a vehicle is declared totaled, the insurance provider takes ownership and pays the agreed-upon value to the insured. Depending on its condition, the insurance company may sell the vehicle to an auction house or a salvage yard.

Once a car is written off, the insurance company takes possession of it and pays the agreed value to the policyholder. The insurance company then sells the car to a salvage yard or an auction house, depending on its condition. If the car is still roadworthy, it may be sold to a new owner willing to repair it.

What Are Your Options if Your Car is Written Off?

If your car is written off, you have a few options:

Accept the payout from the insurance company and use it to buy a new car.

Keep the car and repair it yourself, although this can be expensive.

If you have a lease or finance agreement on the car, you may be able to use the payout from the insurance company to pay off the remaining balance.

Are you looking for reliable comprehensive car insurance or third party fire & theft cover Then get a quote online today or call us at 01 409 2600 to speak to one of our team members.

Frequently Asked Questions About What Does Car Write Offs

Can I buy back my written-off car?

Yes, in some cases, insurance companies allow policyholders to buy back their written-off vehicles, especially if they fall under categories C or D.

How does a write-off affect my insurance premium?

Having a write-off claim can increase your insurance premium as it might categorize you as a higher risk.

Can I dispute a write-off decision?

Yes, if you disagree with the insurance company’s assessment, you can obtain an independent evaluation and discuss it with your insurer.

How is the payout value determined for a written-off car?

The payout is typically based on the car’s market value before the accident, minus any excess or deductible.

What should I do with my car’s documents after it’s written off?

It’s essential to notify the relevant transport authority about the write-off and provide any required documents. Your insurance company can guide you through the process.

Can a written-off car be resold?

Cars in categories A and B cannot be returned to the road. However, those in categories C and D can be repaired and resold, but their history will indicate they were once written off.

Looking to Save On Your Car Insurance?

At KennCo, our car insurance cover offers competitive rates and valuable benefits, including a replacement car as standard. Get peace of mind knowing you’re fully covered.

If you’re looking to get your driver’s license in Ireland, one of the first steps you’ll need to take is passing the theory test. This exam is designed to test your knowledge of the rules of the road, and passing it is essential if you want to obtain a learner permit or a full driver’s license. In this blog post, we’ll cover everything you need to know about passing the theory test in Ireland in 2026.

Study the Rules of the Road

The first step to passing the theory test is to study the Rules of the Road. It is the official publication of the Road Safety Authority (RSA), and it contains all the essential information you need to know to be a safe and responsible driver.

The Rules of the Road is published by the Road Safety Authority (RSA) and has all the information you need to pass your test and become a safe, responsible driver.

The Rules of the Road covers everything from road signs and markings to driving in adverse weather conditions. Ensure you read it thoroughly and pay attention to any sections that you find particularly challenging.

Use Online Resources

In addition to the Rules of the Road, plenty of online resources are available to help you prepare for the theory test.

The RSA website, for example, has a range of practice tests you can take to familiarise yourself with the exam format. There are also several websites and mobile apps that offer similar practice tests, as well as study guides and other helpful resources.

Take Practice Tests

One of the best ways to prepare for the theory test is to take practice tests. These tests are designed to simulate the actual exam, and they can give you a good idea of what to expect on test day. Practice tests can also help you identify areas to study further. Make sure you take as many practice tests as possible before the exam.

Booking a Test

Book a theory test on the RSA’s website. There are numerous nationwide locations, so choose the most convenient for you. From November 2026, stricter rules apply to renewing your learner permit. If you delay your progress, you may be forced to restart the entire process—including sitting the theory test again.

3rd or 4th Permit Renewal: You will not be able to renew your learner permit for a third or fourth time unless you have sat a driving test within the previous two years. Booking a test is no longer enough; you must have actually taken it.

You can take your driver theory test at any test centre in Ireland. There are lots of centres located nationwide so choose one that best suits you.

Arrive Early

On test day, make sure you arrive at the test centre early. Doing so will give you plenty of time to settle in and calm your nerves. You’ll need to bring your learner permit or other identification and proof of payment for the test fee. You’ll also need to sign a declaration stating that you haven’t cheated or received any assistance while preparing for the exam.

Relax and Stay Focused

Finally, it’s important to stay relaxed and focused during the exam. Take deep breaths if you feel anxious, and read each question carefully before answering. Take your time with the questions, and be mindful of the time limit. Remember, you only have 45 minutes to answer 40 questions, so manage your time wisely.

Passing the theory test in Ireland requires preparation, dedication, and focus. Studying the Rules of the Road, using online resources, taking practice tests, arriving early, and staying relaxed and focused can give you the best chance of success.

Theory Test Updates for 2026

In 2026 there are some new rules coming into place around when you must take a Driver Theory Test. again. From November 2026, learner drivers in Ireland will need to successfully complete the theory test again if they:

Have not taken a driving test in the past 2 years and are applying for a third or fourth learner permit.

Have already had four learner permits, there will be no fifth permit allowed (unless there were medical grounds or you were medically restricted).

Held an expired learner permit for 2 years or more.

Applying for a Learners Permit

You will receive a pass certificate when you pass your theory test. This certificate is an important document you’ll need when applying for your learner permit. You must keep it safe and in good condition, as it proves that you’ve successfully passed the theory test.

It’s important to note that the pass certificate is only valid for two years from the date you passed the test. So, it would be best if you used this time to continue working towards obtaining your full driver’s license. Stay motivated; gaining the experience and skills to pass your driving test can take some time.

Passing your theory test is just one step towards becoming a safe and responsible driver. Taking driving lessons, practising regularly, and gaining experience on the road are essential. By doing so, you’ll be well on your way towards obtaining your full driver’s license and enjoying the freedom that comes with it.

At KennCo, we understand that it can be hard for young drivers to get their first car on the road. That’s why we offer low-cost and reliable young driver car insurance.

Frequently Asked Questions How to Pass the Theory Test in 2026

What Is the Driving Theory Test?

The driver theory test is an assessment for learner drivers designed to test their knowledge of road safety and driving regulations. It includes multiple-choice questions and a hazard perception test. You need to pass your theory test if you want to obtain a learner’s permit or full driver’s license.

Can I Study for the Theory Test?

Yes, you can study for the theory test by reading the official Rules of the Road, published by the RSA. There are also online resources available that will allow you to take practice tests to prepare.

Where Can I Find the Rules of the Road?

The Rules of the Road is available from the RSA website or printed copies can be found in most bookshops.

How Do I Book a Theory Test?

You can book your theory test online via the RSA website or by contacting the Driver Theory Test Service on 0818 606 106 (English) or 0818 606 806 (Irish). For security reasons, the RSA recommends only booking your driver theory test through the official RSA website as other websites are fraudulent.

When Will I Find Out If I Passed My Theory Test?

Once you complete the test, your result will be displayed on screen showing whether you passed or failed. A link with your results will also be sent to you via email (using whatever email address provided on your booking). The report with your results will show the specific areas and questions where you answered correctly or incorrectly.

What Happens After Passing the Theory Test?

After passing your theory test, you can apply for your learner permit and start driving lessons with a qualified instructor in order to gain your full driver’s license.

If I Fail, How Long Do I Have to Wait To Take The Theory Test Again?

If you fail your theory test, the RSA advise that you wait at least 3 full business days before taking the test again. This is to give you time to revise and study the areas where you answered incorrectly.

Is There a Limit To How Many Times I Can Take the Theory Test?

No, there are no limits on how many times you can take the theory test.

How many questions do I need to get right to pass the Theory Test?

For the standard categories AM or BW you need to answer 35 out of 40 questions correctly to pass, with 45 minutes to complete it. However, the timeframe and number of questions depends on the your Driver Theory Test category so check your specific category before taking the test.

Q. What to Do If You’ve Put the Wrong Fuel in Your Car

A.

We’ve all had those moments where we weren’t paying attention to a task we were doing. Sometimes it can happen at the petrol station. If you’ve accidentally put the wrong fuel in your car, don’t worry – you’re not alone.

In Ireland, this happens to thousands of motorists every year. But it’s important to act quickly to avoid any potential damage to your vehicle. In this post, we’ll guide you through the steps to take if you’ve put the wrong fuel in your car.

Don’t Start the Engine

If you realise that you’ve put the wrong fuel in your car, you should first avoid starting the engine. Starting the engine will circulate the incorrect fuel throughout the engine, potentially causing severe damage. Instead, remain calm and turn off the ignition if you’ve accidentally switched it on.

Inform the Petrol Station Staff

Once you’ve ensured your engine is off, inform the petrol station staff about your mistake. They are well used to this and can offer assistance or advice on steps to take.

Call a Breakdown Service

In Ireland, various breakdown services can help when you’ve put the wrong fuel in your car. Some insurance companies offer dedicated fuel assist services that can drain and clean your fuel system on-site. Be sure to explain your situation clearly, including the fuel you’ve mistakenly used, so that they can provide the best possible assistance.

Don’t Attempt to Drain the Fuel Yourself

While you may want to try and resolve the issue yourself, draining the fuel system is a job best left to professionals. Doing it yourself can be dangerous and could result in further damage to your car or harm to yourself. Hang on tight, and the problem will get solved.

Check Your Insurance Policy

Some car insurance policies in Ireland include coverage for misfuelling incidents. Contacting your insurance provider to determine if your policy covers this situation is a good idea. They can guide you on the next steps and any potential claim you may need to make.

Get Your Car Checked by a Mechanic

After the wrong fuel has been drained from your car, it’s essential to have a professional mechanic inspect your vehicle. They will be able to assess if any damage has been caused. If it has, they can then recommend necessary repairs. It may be costly, but you’re better off getting it checked before it worsens. Even if your car seems to be running fine after the fuel has been drained, it’s better to be safe than sorry.

Petrol in a Diesel Car vs. Diesel in a Petrol Car: What’s the Difference?

While both scenarios are problematic, putting petrol into a diesel car is generally the more serious and potentially damaging mistake.

Petrol in a Diesel Car: Diesel fuel acts as a lubricant for the fuel pump and other components of the engine. Petrol, on the other hand, has a solvent effect, which can cause significant friction and damage to the fuel pump and injectors if the engine is started. This is often a more costly mistake to rectify.

Diesel in a Petrol Car: This is a less common mistake, as the diesel nozzle is typically larger than the filler neck of a petrol car. If you do manage to put diesel in a petrol car, the engine will likely not start. If it does, it will run poorly, produce a lot of smoke, and quickly cut out. While this can still cause damage, it is generally less severe than the alternative.

Signs You Put The Wrong Fuel In Your Car

If you have driven away from the petrol station and are unsure if you have used the wrong fuel, here are some common symptoms to look out for:

A knocking or pinging sound from the engine, especially when accelerating.

Excessive smoke coming from the exhaust.

Reduced power and sluggish acceleration.

The engine warning light illuminating on your dashboard.

The engine cutting out or failing to start.

If you experience any of these symptoms, you should pull over to a safe place as soon as possible, turn off the engine, and call for breakdown assistance.

The Last Word

Putting the wrong fuel in your car can be a quick mistake but stressful. Taking the proper steps can help minimise any potential damage. Remember, acting quickly and seeking professional help is essential to ensure your vehicle is safe and running smoothly again. So if you find yourself in this situation in Ireland, follow the steps outlined above and get back on the road as soon as possible.

Looking to Save On Your Car Insurance?

At KennCo, our car insurance cover offers competitive rates and valuable benefits, including a replacement car as standard. Get peace of mind knowing you’re fully covered.

Q. Novice Drivers: How Many Points Can a Novice Driver Get?

A.

As a novice driver in Ireland, you must understand the penalty point rules that apply to you.

Novice drivers are those who have held their first learner permit for less than two years; and are subject to different penalty point rules than fully licensed drivers.

In Ireland, like many other countries, driving behaviour is monitored and regulated through a system of penalty points. These points are added to a driver’s license when they commit specific driving offences. The accumulation of penalty points is intended to deter and penalise dangerous or careless driving.

Usually, if a driver accumulates 12 penalty points within a 3-year period they will be automatically disqualified from driving for 6-months. However, novice drivers (and those who hold learner permits) are subject to a lower threshold of 7 penalty points.

Types of Penalty Point Offences

Accumulating penalty points on your license can affect your car insurance premiums and potentially result in license suspension. The number of penalty points you can receive for a driving offence depends on the type of offence committed. For example, if you are caught speeding, you can receive 3 penalty points and a fixed charge fine of €160. However, this can increase to 5 penalty points and a higher fine on conviction.

In Ireland, Novice drivers (and those who hold learner permits) are subject to a lower threshold of 7 penalty points. Accumulating 7 or more penalty points within your first two years of driving will result in your license being revoked.

Similarly, if you are caught using a mobile phone while driving, you can receive 3 penalty points, and not wearing a seatbelt can also result in 3 penalty points. On the other hand, driving without insurance can result in 5 penalty points.

Novice drivers should also be aware that a failure to properly display their N plate while driving can lead to 2 penalty points and a fine of €120, this can also increase on conviction.

But most important to note is that if you accumulate 7 or more penalty points within your first two years of driving, your license will be revoked. And you will have to reapply for a learner permit.

How it Affects Your Car Insurance Premium

One of the implications of accumulating penalty points is the potential impact on car insurance premiums. Insurers often view points on your driving license as an indicator of increased risk, especially for those new to the road.

Novice drivers with penalty points may face higher insurance premiums. Insurers often view these points as an indicator of increased risk, especially for those new to the road.

Insurance companies use various factors to determine the risk associated with insuring a driver, and one of these factors is the driver’s record of penalty points. Here’s why:

Risk Assessment: Insurance companies operate based on risk assessment. Drivers with penalty points are statistically more likely to be involved in accidents or commit further driving offences. As a result, they are considered a higher risk to insure.

Higher Premiums: Due to the increased risk associated with drivers who have penalty points, insurance companies may charge higher premiums to cover the potential costs of future claims. The more penalty points a driver has, the higher their insurance premium might be.

Incentive for Safe Driving: The potential increase in insurance premiums serves as an additional incentive for drivers to adhere to road safety rules and avoid accumulating penalty points. By driving safely and responsibly, drivers can not only avoid legal penalties but also financial implications in the form of higher insurance costs.

Maintaining a Clean Record: In Ireland, penalty points remain on a driver’s record for a specific period, after which they expire. By avoiding further offences during this period, drivers can ensure that their record remains clean. A clean driving record is often rewarded by insurance companies with more competitive premium rates.

Insurance Market Competition: It’s worth noting that the insurance market in Ireland is competitive. Different insurance providers might have varying policies regarding penalty points and how they affect premiums. Therefore, it’s always a good idea for drivers to shop around and compare quotes, especially if they have penalty points on their record.

Tips for Novice Drivers:

Always adhere to speed limits.

Avoid using mobile phones, even hands-free, while driving.

Regularly review and stay updated with traffic rules.

Summary

Safe driving in Ireland keeps you out of legal trouble and can save you money on insurance.

Novice drivers should follow the rules of the road around penalty points, and avoid committing any driving offences that may result in penalty points. Keep your driving record clean, and your car insurance premiums lower. Remember:

Novice drivers in Ireland are those who have held their first learner permit for less than two years.

They are subject to different penalty point rules than fully licensed drivers.

The number of penalty points a novice driver can receive depends on the type of offence.

If a novice driver accumulates 7 or more penalty points within the first two years of driving, their license will be revoked, and they will need to reapply for a learner permit.

Penalty points can affect car insurance premiums, as drivers with points are seen as higher risk.

How Many Points Can a Novice Driver Get? FAQs

What is a novice driver in Ireland?

A novice driver is someone who has received their first driving licence and is within the first two years of holding that licence.

Why must novice drivers display novice plates?

Novice drivers must display N-plates on their vehicles for two years after receiving their first driving licence. This is to help them gain the necessary experience to become safer drivers. Research indicates that novice drivers are most at risk of accidents in their first two years due to inexperience.

What are the special conditions that apply to novice drivers?

– Novice Drivers must display N-plates on their vehicle for the first two years. – Novice Drivers cannot act as a sponsor or accompanying driver for a category B learner driver. – A lower blood alcohol concentration threshold of 20mg applies to Novice Drivers. – A lower threshold of seven penalty points leading to disqualification applies to Novice Drivers.

What happens if a novice driver accumulates 7 or more penalty points?

If a novice driver accumulates 7 or more penalty points within their first two years of driving, their licence will be revoked, and they will need to reapply for a learner permit.

How do penalty points affect novice drivers’ car insurance premiums?

Insurance companies view drivers with penalty points as higher risk, leading to potentially higher car insurance premiums.

How long do penalty points last on a novice driver’s record?

Penalty points in Ireland expire after a set period. Avoiding new offences means the record clears over time, potentially leading to lower premiums.

Save On Young Driver Car Insurance?

At KennCo, we understand that it can be hard for young drivers to get their first car on the road. That’s why we offer low-cost and reliable young driver car insurance.